Canada x Indo-Pacific [13th Ed.] DSRB to Be Hosted in Canada, Japan’s Export Rule Reforms Continue, CPSP Bid Revisions

May 14, 2026

(Thank you to Asia Pacific Foundation of Canada for the opportunity to co-author the report released on the 14th: Canada Singapore Defence Industrial Cooperation. Also had the pleasure of attending Singapore Maritime Week, there were some impressive innovative firms on the floor and some great pitches.)

Executive Summary

The Carney government’s recent moves, DIA’s CPSP bid revision, CPCSC Level 1 roll out, DSRB host status, and the Automaker-Hanwha tie up, are starting to look less like discrete initiatives and more like coherent application of industrial policy. Outside Canada, the period’s core lessons from allies seems to be that allied defence industrial bases (particularly South Korea and Japan) are reorganizing around export market opportunities and co-production, not just national procurement. At the moment, allies and partners are clearly a step ahead on the export .

Canada secured host status for the new Defence, Security and Resilience Bank, positioning Ottawa as a financing hub for allied supply chains. The implications for partners on this side of the planet are unclear as of yet. PSPC launched CP-CSC Level 1, upping the compliance bar for the supplier base. Japan delivered the period’s most consequential industrial outcomes including the scrapping of the five-category export limit on 21 April, and continuing to advance the Mogami contract with Australia for eleven frigates. Together these convert Japan from constrained exporter into a credible supplier of complete weapon systems. South Korea matched the pace: Ottawa allowed Hanwha and TKMS to revise CPSP bids, Korea responded with automotive, sustainment and shipbuilding sweeteners, and Hanwha Ocean signed the Leidos partnership anchoring a long-term North American footprint in design and engineering. In addition, the KF-21 Boramae completed its serial-production maiden flight. Australia released its 2026 National Defence Strategy at AUD 425 billion over the decade. Singapore cut steel on the third and fourth MRCV, and Canada participated in Exercise Balikatan in the Philippines for the first time.

Summary of What to Watch

Immediate (Next 30 Days)

- CPSP bid revision evaluation. Anticipate one or two surprise announcements in the home stretch as evaluators work through finalised bids.

- DSRB capital commitments. Canada secured the host mandate. The live questions are which partner countries commit capital and how DSRB differentiates from existing export-import arrangements.

- CP-CSC SME onboarding supports. Watch for announcements around financial or other supports as SMEs work to onboard CP-CSC.

Medium-Term (2026)

- Team Canada Trade Mission to Japan in June. First concrete test of whether Canadian firms get matched with the Japanese trading houses and primes on co-production conversations rather than the standard sales-pitch format. Made more interesting by the new Japanese export posture.

- Korea’s export-strategy adjustments. Whether Seoul restructures its export apparatus in response to recent setbacks, or pushes through with the current playbook.

Strategic (2026+)

- Japan as complete-systems exporter. The 21 April rule change makes Japan a serious competitor in Indonesian, Vietnamese and Filipino procurement competitions.

CANADA: DSRB to be Hosted in Canada, CP-CSC Rolls Out, Carney's Indo-Pacific Strategy Year One

- Carney’s Indo-Pacific posture, one year in. APF Canada’s Vina Nadjibulla in Policy Magazine argues Canada’s regional footprint is stronger than ever, but the DIS still runs industrial cooperation almost entirely through NATO channels, leaving an Indo-Pacific gap to close.

- CP-CSC Introduction: the Canadian Program for Cyber Security Certificationlaunched 14 April. Defenders frame the policy as a long-overdue clean-up of the supply chain’s cyber posture. Critics counter that the compliance overhead lands hardest on SMEs without dedicated security staff, and risks narrowing the supplier pool at the moment Ottawa is trying to widen it. PSPC has signalled a phased rollout starting with Level 1; the live test will be transition timing for incumbents on active contracts.

- DSRB headquarters bid lands in Canada. Charter negotiations concluded in Montréal on 29 April, with Canada positioning to host a new multilateral bank for defence supply-chain financing. Open questions: are Japan, Korea, and Australia in or out, and how does the DSRB sit alongside JBIC, KEXIM, and EFA?

Watch: Three open files. Does Tokyo, Seoul or Canberra commit capital to DSRB, and where does it sit relative to JBIC, KEXIM and EFA? Does CP-CSC Level 1 get a transition window for SME incumbents, or land as a hard cut-over? Will Operation Neon continue?

JAPAN: Export Rules Loosened, Mogami Contract Signed, Team Canada Eyes Tokyo

- Export rules loosened. Tokyo scrapped the five-category limit on defence exports on 21 April, shifting from the rescue, transport, surveillance, warning and mine-sweeping list to case-by-case review. Early implications include New Zealand’s evaluation of the Mogami class, renewed Southeast Asia interest and strong indications that Ukraine is exploring sourcing from Japan.

• Updated Free and Open Indo-Pacific Policy: Japan released its updated Free and Open Indo-Pacific policy on 2 May 2026, with Prime Minister Takaichi announcing the refresh in Hanoi under the banner of making the region “more resilient and prosperous together.” - Mogami contract signed. Australia and Japan executed binding contracts on 18 April for eleven Mogami-class frigates worth roughly USD 7 billion, with Defence Minister Richard Marles and Japanese counterpart Shinjiro Koizumi formalising the largest defence export in Japan’s modern history. The deal anchors MHI as the lead non-US naval supplier to Australia and gives Tokyo a working template for selling complete platforms abroad. Engagements also included signature of a critical mineral arrangement likely in response to Chinese sanctions.

- Team Canada trade mission to Japan in June. Global Affairs has flagged a June trade mission that should feature a defence and security stream. With export rules just loosened, the practical question is whether Canadian firms get matched with the trading houses (Marubeni, Mitsubishi, Sumitomo) and primes (MHI, KHI, Toshiba) on co-production or supply-chain conversations rather than the usual sales-pitch format.

Watch: Does the June trade mission produce real bilateral defence-industrial frameworks, now that the information sharing agreement is in place? Does NZ’s Mogami consideration mature into a formal acquisition pathway? How does this impact the competitive space?

SOUTH KOREA: CPSP Bid Revisions Land, Hanwha’s Canadian Partner Web Expands, KF-21 Hits Milestone

- CPSP bid revisions land. Ottawa allowed Hanwha and TKMS to revise CPSP bids, and Korea responded with industrial sweeteners. Hanwha would partner with Canadian automotive parts manufacturers, pitched against the backdrop of Canada’s struggling automotive sector under US tariff exposure. Reporting also detailed some of the CPSP scoring and weighting: platform 20 percent, financial criteria 15 percent, with sustainment at 50% carrying the dominant weight. TKMS has countered by pointing to partnerships with Bombardier and Lockheed Martin.

- Hanwha’s Canadian partner web expands. Hanwha Ocean has announced cooperation frameworks with Irving Shipbuilding, AtkinsRéalis, Boreal Energy Systems and Magellan Aerospace. The Irving framework extends beyond builder-supplier into sustainment and workforce. As DIA CEO states that bidders should ‘think hard about whether you have more to put on the table.’

- KF-21 Boramae completes maiden flight. The first serial-production KF-21 completed its maiden flight 22 days after rollout. The milestone matters for KAI and the broader Korean aerospace export pitch into Southeast Asia and the Middle East.

- Hanwha Ocean’s North American shipbuilding bet. Hanwha Ocean signed a US naval design partnership with Leidos, and announced a Philadelphia shipyard workforce expansion on 27 April. The combination positions Hanwha as a long-term player in the US naval shipbuilding gap. Headwinds remain in global markets, including losses on Australia’s frigate competition, friction on Poland’s Orka submarine programme, and US execution risk. The counter argument is that these examples are noise against a structural boom.

Watch: Do recent export setbacks force structural changes to Korea’s export strategy and apparatus, or does Seoul push through? Does Hanwha bring the TIGON wheeled APC into a Canadian manufacturing footprint, putting its vehicle portfolio in direct competition with GDLS’s LAV 6.0 line in London? Or does it focus on the heavier tracked IFV segment Redback, closer in capability to the cancelled Close Combat Vehicle programme?

AUSTRALIA: 2026 NDS Released, AUKUS Industrial Base Deepens, Critical Minerals Gambit

- 2026 NDS released. Australia’s 2026 National Defence Strategy commits AUD 425 billion over the decade, including AUD 53 billion in additional funding. Priorities: undersea warfare, maritime lethality, long-range strike, integrated air and missile defence, autonomous and uncrewed systems, counter-UAS, resilient multi-orbit satcom. Five pillars: greater self-reliance, capability lessons from Ukraine and the Middle East, sovereign defence industrial base resilience, civil preparedness and economic security, regional coordination. The NDS’s emphasis on uncrewed systems, counter-UAS, air and missile defence, and long-range strike shows Canberra converting battlefield lessons from Ukraine and the Middle East into procurement and domestic industrial priorities.

- AUKUS as industrial base. A Global Economics analysis frames AUKUS as evolving from a platform deal into a trilateral defence-industrial base, citing the Ghost Shark autonomous underwater vehicle programme as evidence of how AUKUS is converging defence with advanced manufacturing in Australia, with dozens of local firms now in the supply chain.

Watch: How will Australia’s forthcoming defense industrial strategies adapt or operationalize the national defense strategy?

Other Regional Development

- Taiwan: NCSIST will cooperate with Saronic Technologies and Maritime Tactical Systems on uncrewed surface vessels. Taiwan continues to make inroads in global export markets, particularly for drones. In the U.S. where green or blue UAS certification is required for procurement there seems to have been a breakthrough. Germany is advancing defence partnerships with Taiwan, while Canada faces direct warnings from the Chinese envoy on Taiwan-related engagement.

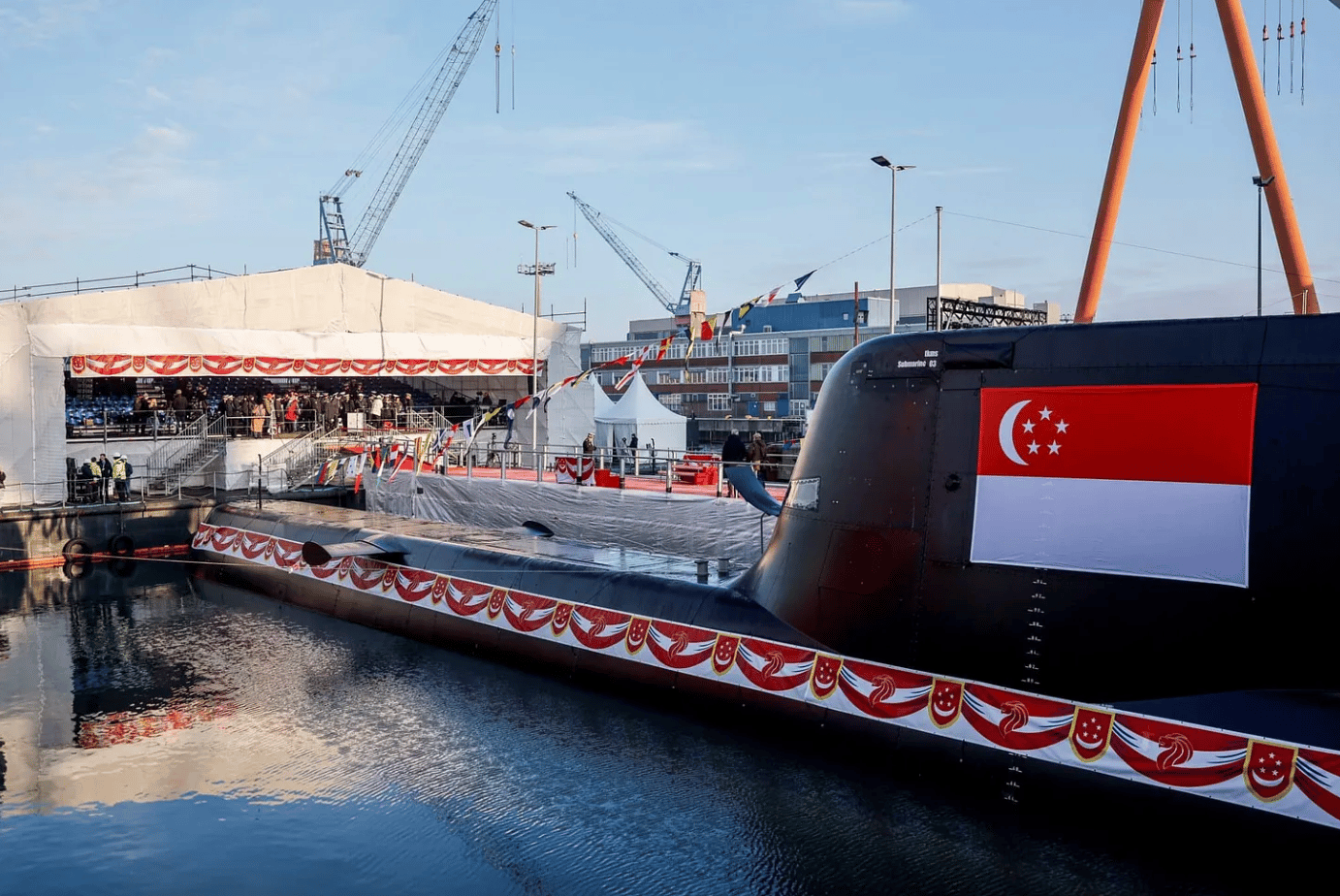

- Singapore: RSN held the steel-cutting ceremony for the third and fourth MRCV. At 150 metres, 8,000 tonnes, 22 knots and over 7,000 nautical miles range, MRCVs are the largest and most technically sophisticated warships built in Singapore. Singapore also announced plans for its first dedicated public safety satellite, Xplorer, scheduled for launch in 2029. ST Engineering announced S4.8 billion in contract awards in Q1 2026, concentrated in the Middle East (Qatar, UAE, Kuwait). Pier 71 launched the SmartPort Challenge at Maritime Week, and Singapore hosted the Milipol TechX trade show.

- Philippines: Exercise Balikatan, running 28 April to 8 May, is one of the largest in its history, with 17,000 personnel including the US, Philippines, Japan, Australia, Canada, France and New Zealand. Canada participated for the first time.

Source: Linkedin, Canada’s Ambassador to the Philippines

- India: Modi and South Korea’s President agreed to expand defence cooperation beyond the K-9, naming missile systems and anti-aircraft guns, and launched the Korea-India Defence Accelerator Innovation Platform. India also signed a bilateral pact with Russia covering troop and warship deployment, deepening the partnership despite declining Russian arms exports to India.

- New Zealand: Participation in Balikatan and P-8A operations underscore regional demand for maritime patrol, in particular for enforcement of sanctions.

Key Upcoming Events

- The New Maritime Battlespace | 5 May | St. John, NB

- AUSA LANPAC | 12-14 May | Honolulu

- Indian Ocean Defence & Security | 26-28 May | Perth

- CANSEC 2026 | 27-28 May | Ottawa

- Shangri-La Dialogue | 29-31 May | Singapore

- Critical Minerals for Defence | 9-10 June | Toronto

- Naval Defense Philippines | 17-19 June | Manila

- ADSE 2026 | 6-7 August | Abbotsford, BC

- Canadian Aerospace Summit | 27-28 October | Ottawa

Other Insights

Canada x IndoPacific [15th Ed.] - Submarine Endgame in Ankara (?), Huge International Acquisition by Canadian Firm, Not So Glorious (But Important) Paperwork & Agreements Move Forward

July 2, 2026

Canada x Indo-Pacific [14th Ed.] Summit Season in Beijing, Wang Yi in Ottawa, CPSP End of the Beginning, Biggest CANSEC Ever

June 4, 2026

Canada x Indo-Pacific [13th Ed.] DSRB to Be Hosted in Canada, Japan’s Export Rule Reforms Continue, CPSP Bid Revisions

May 14, 2026

Defence Market Intelligence for Strategic Autonomy

© 2026 PerceptX Inc.

Canada x Indo-Pacific [13th Ed.] DSRB to Be Hosted in Canada, Japan’s Export Rule Reforms Continue, CPSP Bid Revisions

May 14, 2026

(Thank you to Asia Pacific Foundation of Canada for the opportunity to co-author the report released on the 14th: Canada Singapore Defence Industrial Cooperation. Also had the pleasure of attending Singapore Maritime Week, there were some impressive innovative firms on the floor and some great pitches.)

Executive Summary

The Carney government’s recent moves, DIA’s CPSP bid revision, CPCSC Level 1 roll out, DSRB host status, and the Automaker-Hanwha tie up, are starting to look less like discrete initiatives and more like coherent application of industrial policy. Outside Canada, the period’s core lessons from allies seems to be that allied defence industrial bases (particularly South Korea and Japan) are reorganizing around export market opportunities and co-production, not just national procurement. At the moment, allies and partners are clearly a step ahead on the export .

Canada secured host status for the new Defence, Security and Resilience Bank, positioning Ottawa as a financing hub for allied supply chains. The implications for partners on this side of the planet are unclear as of yet. PSPC launched CP-CSC Level 1, upping the compliance bar for the supplier base. Japan delivered the period’s most consequential industrial outcomes including the scrapping of the five-category export limit on 21 April, and continuing to advance the Mogami contract with Australia for eleven frigates. Together these convert Japan from constrained exporter into a credible supplier of complete weapon systems. South Korea matched the pace: Ottawa allowed Hanwha and TKMS to revise CPSP bids, Korea responded with automotive, sustainment and shipbuilding sweeteners, and Hanwha Ocean signed the Leidos partnership anchoring a long-term North American footprint in design and engineering. In addition, the KF-21 Boramae completed its serial-production maiden flight. Australia released its 2026 National Defence Strategy at AUD 425 billion over the decade. Singapore cut steel on the third and fourth MRCV, and Canada participated in Exercise Balikatan in the Philippines for the first time.

Summary of What to Watch

Immediate (Next 30 Days)

- CPSP bid revision evaluation. Anticipate one or two surprise announcements in the home stretch as evaluators work through finalised bids.

- DSRB capital commitments. Canada secured the host mandate. The live questions are which partner countries commit capital and how DSRB differentiates from existing export-import arrangements.

- CP-CSC SME onboarding supports. Watch for announcements around financial or other supports as SMEs work to onboard CP-CSC.

Medium-Term (2026)

- Team Canada Trade Mission to Japan in June. First concrete test of whether Canadian firms get matched with the Japanese trading houses and primes on co-production conversations rather than the standard sales-pitch format. Made more interesting by the new Japanese export posture.

- Korea’s export-strategy adjustments. Whether Seoul restructures its export apparatus in response to recent setbacks, or pushes through with the current playbook.

Strategic (2026+)

- Japan as complete-systems exporter. The 21 April rule change makes Japan a serious competitor in Indonesian, Vietnamese and Filipino procurement competitions.

CANADA: DSRB to be Hosted in Canada, CP-CSC Rolls Out, Carney's Indo-Pacific Strategy Year One

- Carney’s Indo-Pacific posture, one year in. APF Canada’s Vina Nadjibulla in Policy Magazine argues Canada’s regional footprint is stronger than ever, but the DIS still runs industrial cooperation almost entirely through NATO channels, leaving an Indo-Pacific gap to close.

- CP-CSC Introduction: the Canadian Program for Cyber Security Certificationlaunched 14 April. Defenders frame the policy as a long-overdue clean-up of the supply chain’s cyber posture. Critics counter that the compliance overhead lands hardest on SMEs without dedicated security staff, and risks narrowing the supplier pool at the moment Ottawa is trying to widen it. PSPC has signalled a phased rollout starting with Level 1; the live test will be transition timing for incumbents on active contracts.

- DSRB headquarters bid lands in Canada. Charter negotiations concluded in Montréal on 29 April, with Canada positioning to host a new multilateral bank for defence supply-chain financing. Open questions: are Japan, Korea, and Australia in or out, and how does the DSRB sit alongside JBIC, KEXIM, and EFA?

Watch: Three open files. Does Tokyo, Seoul or Canberra commit capital to DSRB, and where does it sit relative to JBIC, KEXIM and EFA? Does CP-CSC Level 1 get a transition window for SME incumbents, or land as a hard cut-over? Will Operation Neon continue?

JAPAN: Export Rules Loosened, Mogami Contract Signed, Team Canada Eyes Tokyo

- Export rules loosened. Tokyo scrapped the five-category limit on defence exports on 21 April, shifting from the rescue, transport, surveillance, warning and mine-sweeping list to case-by-case review. Early implications include New Zealand’s evaluation of the Mogami class, renewed Southeast Asia interest and strong indications that Ukraine is exploring sourcing from Japan.

• Updated Free and Open Indo-Pacific Policy: Japan released its updated Free and Open Indo-Pacific policy on 2 May 2026, with Prime Minister Takaichi announcing the refresh in Hanoi under the banner of making the region “more resilient and prosperous together.” - Mogami contract signed. Australia and Japan executed binding contracts on 18 April for eleven Mogami-class frigates worth roughly USD 7 billion, with Defence Minister Richard Marles and Japanese counterpart Shinjiro Koizumi formalising the largest defence export in Japan’s modern history. The deal anchors MHI as the lead non-US naval supplier to Australia and gives Tokyo a working template for selling complete platforms abroad. Engagements also included signature of a critical mineral arrangement likely in response to Chinese sanctions.

- Team Canada trade mission to Japan in June. Global Affairs has flagged a June trade mission that should feature a defence and security stream. With export rules just loosened, the practical question is whether Canadian firms get matched with the trading houses (Marubeni, Mitsubishi, Sumitomo) and primes (MHI, KHI, Toshiba) on co-production or supply-chain conversations rather than the usual sales-pitch format.

Watch: Does the June trade mission produce real bilateral defence-industrial frameworks, now that the information sharing agreement is in place? Does NZ’s Mogami consideration mature into a formal acquisition pathway? How does this impact the competitive space?

SOUTH KOREA: CPSP Bid Revisions Land, Hanwha’s Canadian Partner Web Expands, KF-21 Hits Milestone

- CPSP bid revisions land. Ottawa allowed Hanwha and TKMS to revise CPSP bids, and Korea responded with industrial sweeteners. Hanwha would partner with Canadian automotive parts manufacturers, pitched against the backdrop of Canada’s struggling automotive sector under US tariff exposure. Reporting also detailed some of the CPSP scoring and weighting: platform 20 percent, financial criteria 15 percent, with sustainment at 50% carrying the dominant weight. TKMS has countered by pointing to partnerships with Bombardier and Lockheed Martin.

- Hanwha’s Canadian partner web expands. Hanwha Ocean has announced cooperation frameworks with Irving Shipbuilding, AtkinsRéalis, Boreal Energy Systems and Magellan Aerospace. The Irving framework extends beyond builder-supplier into sustainment and workforce. As DIA CEO states that bidders should ‘think hard about whether you have more to put on the table.’

- KF-21 Boramae completes maiden flight. The first serial-production KF-21 completed its maiden flight 22 days after rollout. The milestone matters for KAI and the broader Korean aerospace export pitch into Southeast Asia and the Middle East.

- Hanwha Ocean’s North American shipbuilding bet. Hanwha Ocean signed a US naval design partnership with Leidos, and announced a Philadelphia shipyard workforce expansion on 27 April. The combination positions Hanwha as a long-term player in the US naval shipbuilding gap. Headwinds remain in global markets, including losses on Australia’s frigate competition, friction on Poland’s Orka submarine programme, and US execution risk. The counter argument is that these examples are noise against a structural boom.

Watch: Do recent export setbacks force structural changes to Korea’s export strategy and apparatus, or does Seoul push through? Does Hanwha bring the TIGON wheeled APC into a Canadian manufacturing footprint, putting its vehicle portfolio in direct competition with GDLS’s LAV 6.0 line in London? Or does it focus on the heavier tracked IFV segment Redback, closer in capability to the cancelled Close Combat Vehicle programme?

AUSTRALIA: 2026 NDS Released, AUKUS Industrial Base Deepens, Critical Minerals Gambit

- 2026 NDS released. Australia’s 2026 National Defence Strategy commits AUD 425 billion over the decade, including AUD 53 billion in additional funding. Priorities: undersea warfare, maritime lethality, long-range strike, integrated air and missile defence, autonomous and uncrewed systems, counter-UAS, resilient multi-orbit satcom. Five pillars: greater self-reliance, capability lessons from Ukraine and the Middle East, sovereign defence industrial base resilience, civil preparedness and economic security, regional coordination. The NDS’s emphasis on uncrewed systems, counter-UAS, air and missile defence, and long-range strike shows Canberra converting battlefield lessons from Ukraine and the Middle East into procurement and domestic industrial priorities.

- AUKUS as industrial base. A Global Economics analysis frames AUKUS as evolving from a platform deal into a trilateral defence-industrial base, citing the Ghost Shark autonomous underwater vehicle programme as evidence of how AUKUS is converging defence with advanced manufacturing in Australia, with dozens of local firms now in the supply chain.

Watch: How will Australia’s forthcoming defense industrial strategies adapt or operationalize the national defense strategy?

Other Regional Development

- Taiwan: NCSIST will cooperate with Saronic Technologies and Maritime Tactical Systems on uncrewed surface vessels. Taiwan continues to make inroads in global export markets, particularly for drones. In the U.S. where green or blue UAS certification is required for procurement there seems to have been a breakthrough. Germany is advancing defence partnerships with Taiwan, while Canada faces direct warnings from the Chinese envoy on Taiwan-related engagement.

- Singapore: RSN held the steel-cutting ceremony for the third and fourth MRCV. At 150 metres, 8,000 tonnes, 22 knots and over 7,000 nautical miles range, MRCVs are the largest and most technically sophisticated warships built in Singapore. Singapore also announced plans for its first dedicated public safety satellite, Xplorer, scheduled for launch in 2029. ST Engineering announced S4.8 billion in contract awards in Q1 2026, concentrated in the Middle East (Qatar, UAE, Kuwait). Pier 71 launched the SmartPort Challenge at Maritime Week, and Singapore hosted the Milipol TechX trade show.

- Philippines: Exercise Balikatan, running 28 April to 8 May, is one of the largest in its history, with 17,000 personnel including the US, Philippines, Japan, Australia, Canada, France and New Zealand. Canada participated for the first time.

Source: Linkedin, Canada’s Ambassador to the Philippines

- India: Modi and South Korea’s President agreed to expand defence cooperation beyond the K-9, naming missile systems and anti-aircraft guns, and launched the Korea-India Defence Accelerator Innovation Platform. India also signed a bilateral pact with Russia covering troop and warship deployment, deepening the partnership despite declining Russian arms exports to India.

- New Zealand: Participation in Balikatan and P-8A operations underscore regional demand for maritime patrol, in particular for enforcement of sanctions.

Key Upcoming Events

- The New Maritime Battlespace | 5 May | St. John, NB

- AUSA LANPAC | 12-14 May | Honolulu

- Indian Ocean Defence & Security | 26-28 May | Perth

- CANSEC 2026 | 27-28 May | Ottawa

- Shangri-La Dialogue | 29-31 May | Singapore

- Critical Minerals for Defence | 9-10 June | Toronto

- Naval Defense Philippines | 17-19 June | Manila

- ADSE 2026 | 6-7 August | Abbotsford, BC

- Canadian Aerospace Summit | 27-28 October | Ottawa

Other Insights

Canada x IndoPacific [15th Ed.] - Submarine Endgame in Ankara (?), Huge International Acquisition by Canadian Firm, Not So Glorious (But Important) Paperwork & Agreements Move Forward

July 2, 2026

Canada x Indo-Pacific [14th Ed.] Summit Season in Beijing, Wang Yi in Ottawa, CPSP End of the Beginning, Biggest CANSEC Ever

June 4, 2026

Canada x Indo-Pacific [13th Ed.] DSRB to Be Hosted in Canada, Japan’s Export Rule Reforms Continue, CPSP Bid Revisions

May 14, 2026

Defence Market Intelligence for Strategic Autonomy

© 2026 PerceptX Inc.

about

services

Capabilities

News

contact us

Canada x Indo-Pacific [13th Ed.] DSRB to Be Hosted in Canada, Japan’s Export Rule Reforms Continue, CPSP Bid Revisions

May 14, 2026

(Thank you to Asia Pacific Foundation of Canada for the opportunity to co-author the report released on the 14th: Canada Singapore Defence Industrial Cooperation. Also had the pleasure of attending Singapore Maritime Week, there were some impressive innovative firms on the floor and some great pitches.)

Executive Summary

The Carney government’s recent moves, DIA’s CPSP bid revision, CPCSC Level 1 roll out, DSRB host status, and the Automaker-Hanwha tie up, are starting to look less like discrete initiatives and more like coherent application of industrial policy. Outside Canada, the period’s core lessons from allies seems to be that allied defence industrial bases (particularly South Korea and Japan) are reorganizing around export market opportunities and co-production, not just national procurement. At the moment, allies and partners are clearly a step ahead on the export .

Canada secured host status for the new Defence, Security and Resilience Bank, positioning Ottawa as a financing hub for allied supply chains. The implications for partners on this side of the planet are unclear as of yet. PSPC launched CP-CSC Level 1, upping the compliance bar for the supplier base. Japan delivered the period’s most consequential industrial outcomes including the scrapping of the five-category export limit on 21 April, and continuing to advance the Mogami contract with Australia for eleven frigates. Together these convert Japan from constrained exporter into a credible supplier of complete weapon systems. South Korea matched the pace: Ottawa allowed Hanwha and TKMS to revise CPSP bids, Korea responded with automotive, sustainment and shipbuilding sweeteners, and Hanwha Ocean signed the Leidos partnership anchoring a long-term North American footprint in design and engineering. In addition, the KF-21 Boramae completed its serial-production maiden flight. Australia released its 2026 National Defence Strategy at AUD 425 billion over the decade. Singapore cut steel on the third and fourth MRCV, and Canada participated in Exercise Balikatan in the Philippines for the first time.

Summary of What to Watch

Immediate (Next 30 Days)

- CPSP bid revision evaluation. Anticipate one or two surprise announcements in the home stretch as evaluators work through finalised bids.

- DSRB capital commitments. Canada secured the host mandate. The live questions are which partner countries commit capital and how DSRB differentiates from existing export-import arrangements.

- CP-CSC SME onboarding supports. Watch for announcements around financial or other supports as SMEs work to onboard CP-CSC.

Medium-Term (2026)

- Team Canada Trade Mission to Japan in June. First concrete test of whether Canadian firms get matched with the Japanese trading houses and primes on co-production conversations rather than the standard sales-pitch format. Made more interesting by the new Japanese export posture.

- Korea’s export-strategy adjustments. Whether Seoul restructures its export apparatus in response to recent setbacks, or pushes through with the current playbook.

Strategic (2026+)

- Japan as complete-systems exporter. The 21 April rule change makes Japan a serious competitor in Indonesian, Vietnamese and Filipino procurement competitions.

CANADA: DSRB to be Hosted in Canada, CP-CSC Rolls Out, Carney's Indo-Pacific Strategy Year One

- Carney’s Indo-Pacific posture, one year in. APF Canada’s Vina Nadjibulla in Policy Magazine argues Canada’s regional footprint is stronger than ever, but the DIS still runs industrial cooperation almost entirely through NATO channels, leaving an Indo-Pacific gap to close.

- CP-CSC Introduction: the Canadian Program for Cyber Security Certificationlaunched 14 April. Defenders frame the policy as a long-overdue clean-up of the supply chain’s cyber posture. Critics counter that the compliance overhead lands hardest on SMEs without dedicated security staff, and risks narrowing the supplier pool at the moment Ottawa is trying to widen it. PSPC has signalled a phased rollout starting with Level 1; the live test will be transition timing for incumbents on active contracts.

- DSRB headquarters bid lands in Canada. Charter negotiations concluded in Montréal on 29 April, with Canada positioning to host a new multilateral bank for defence supply-chain financing. Open questions: are Japan, Korea, and Australia in or out, and how does the DSRB sit alongside JBIC, KEXIM, and EFA?

Watch: Three open files. Does Tokyo, Seoul or Canberra commit capital to DSRB, and where does it sit relative to JBIC, KEXIM and EFA? Does CP-CSC Level 1 get a transition window for SME incumbents, or land as a hard cut-over? Will Operation Neon continue?

JAPAN: Export Rules Loosened, Mogami Contract Signed, Team Canada Eyes Tokyo

- Export rules loosened. Tokyo scrapped the five-category limit on defence exports on 21 April, shifting from the rescue, transport, surveillance, warning and mine-sweeping list to case-by-case review. Early implications include New Zealand’s evaluation of the Mogami class, renewed Southeast Asia interest and strong indications that Ukraine is exploring sourcing from Japan.

• Updated Free and Open Indo-Pacific Policy: Japan released its updated Free and Open Indo-Pacific policy on 2 May 2026, with Prime Minister Takaichi announcing the refresh in Hanoi under the banner of making the region “more resilient and prosperous together.” - Mogami contract signed. Australia and Japan executed binding contracts on 18 April for eleven Mogami-class frigates worth roughly USD 7 billion, with Defence Minister Richard Marles and Japanese counterpart Shinjiro Koizumi formalising the largest defence export in Japan’s modern history. The deal anchors MHI as the lead non-US naval supplier to Australia and gives Tokyo a working template for selling complete platforms abroad. Engagements also included signature of a critical mineral arrangement likely in response to Chinese sanctions.

- Team Canada trade mission to Japan in June. Global Affairs has flagged a June trade mission that should feature a defence and security stream. With export rules just loosened, the practical question is whether Canadian firms get matched with the trading houses (Marubeni, Mitsubishi, Sumitomo) and primes (MHI, KHI, Toshiba) on co-production or supply-chain conversations rather than the usual sales-pitch format.

Watch: Does the June trade mission produce real bilateral defence-industrial frameworks, now that the information sharing agreement is in place? Does NZ’s Mogami consideration mature into a formal acquisition pathway? How does this impact the competitive space?

SOUTH KOREA: CPSP Bid Revisions Land, Hanwha’s Canadian Partner Web Expands, KF-21 Hits Milestone

- CPSP bid revisions land. Ottawa allowed Hanwha and TKMS to revise CPSP bids, and Korea responded with industrial sweeteners. Hanwha would partner with Canadian automotive parts manufacturers, pitched against the backdrop of Canada’s struggling automotive sector under US tariff exposure. Reporting also detailed some of the CPSP scoring and weighting: platform 20 percent, financial criteria 15 percent, with sustainment at 50% carrying the dominant weight. TKMS has countered by pointing to partnerships with Bombardier and Lockheed Martin.

- Hanwha’s Canadian partner web expands. Hanwha Ocean has announced cooperation frameworks with Irving Shipbuilding, AtkinsRéalis, Boreal Energy Systems and Magellan Aerospace. The Irving framework extends beyond builder-supplier into sustainment and workforce. As DIA CEO states that bidders should ‘think hard about whether you have more to put on the table.’

- KF-21 Boramae completes maiden flight. The first serial-production KF-21 completed its maiden flight 22 days after rollout. The milestone matters for KAI and the broader Korean aerospace export pitch into Southeast Asia and the Middle East.

- Hanwha Ocean’s North American shipbuilding bet. Hanwha Ocean signed a US naval design partnership with Leidos, and announced a Philadelphia shipyard workforce expansion on 27 April. The combination positions Hanwha as a long-term player in the US naval shipbuilding gap. Headwinds remain in global markets, including losses on Australia’s frigate competition, friction on Poland’s Orka submarine programme, and US execution risk. The counter argument is that these examples are noise against a structural boom.

Watch: Do recent export setbacks force structural changes to Korea’s export strategy and apparatus, or does Seoul push through? Does Hanwha bring the TIGON wheeled APC into a Canadian manufacturing footprint, putting its vehicle portfolio in direct competition with GDLS’s LAV 6.0 line in London? Or does it focus on the heavier tracked IFV segment Redback, closer in capability to the cancelled Close Combat Vehicle programme?

AUSTRALIA: 2026 NDS Released, AUKUS Industrial Base Deepens, Critical Minerals Gambit

- 2026 NDS released. Australia’s 2026 National Defence Strategy commits AUD 425 billion over the decade, including AUD 53 billion in additional funding. Priorities: undersea warfare, maritime lethality, long-range strike, integrated air and missile defence, autonomous and uncrewed systems, counter-UAS, resilient multi-orbit satcom. Five pillars: greater self-reliance, capability lessons from Ukraine and the Middle East, sovereign defence industrial base resilience, civil preparedness and economic security, regional coordination. The NDS’s emphasis on uncrewed systems, counter-UAS, air and missile defence, and long-range strike shows Canberra converting battlefield lessons from Ukraine and the Middle East into procurement and domestic industrial priorities.

- AUKUS as industrial base. A Global Economics analysis frames AUKUS as evolving from a platform deal into a trilateral defence-industrial base, citing the Ghost Shark autonomous underwater vehicle programme as evidence of how AUKUS is converging defence with advanced manufacturing in Australia, with dozens of local firms now in the supply chain.

Watch: How will Australia’s forthcoming defense industrial strategies adapt or operationalize the national defense strategy?

Other Regional Development

- Taiwan: NCSIST will cooperate with Saronic Technologies and Maritime Tactical Systems on uncrewed surface vessels. Taiwan continues to make inroads in global export markets, particularly for drones. In the U.S. where green or blue UAS certification is required for procurement there seems to have been a breakthrough. Germany is advancing defence partnerships with Taiwan, while Canada faces direct warnings from the Chinese envoy on Taiwan-related engagement.

- Singapore: RSN held the steel-cutting ceremony for the third and fourth MRCV. At 150 metres, 8,000 tonnes, 22 knots and over 7,000 nautical miles range, MRCVs are the largest and most technically sophisticated warships built in Singapore. Singapore also announced plans for its first dedicated public safety satellite, Xplorer, scheduled for launch in 2029. ST Engineering announced S4.8 billion in contract awards in Q1 2026, concentrated in the Middle East (Qatar, UAE, Kuwait). Pier 71 launched the SmartPort Challenge at Maritime Week, and Singapore hosted the Milipol TechX trade show.

- Philippines: Exercise Balikatan, running 28 April to 8 May, is one of the largest in its history, with 17,000 personnel including the US, Philippines, Japan, Australia, Canada, France and New Zealand. Canada participated for the first time.

Source: Linkedin, Canada’s Ambassador to the Philippines

- India: Modi and South Korea’s President agreed to expand defence cooperation beyond the K-9, naming missile systems and anti-aircraft guns, and launched the Korea-India Defence Accelerator Innovation Platform. India also signed a bilateral pact with Russia covering troop and warship deployment, deepening the partnership despite declining Russian arms exports to India.

- New Zealand: Participation in Balikatan and P-8A operations underscore regional demand for maritime patrol, in particular for enforcement of sanctions.

Key Upcoming Events

- The New Maritime Battlespace | 5 May | St. John, NB

- AUSA LANPAC | 12-14 May | Honolulu

- Indian Ocean Defence & Security | 26-28 May | Perth

- CANSEC 2026 | 27-28 May | Ottawa

- Shangri-La Dialogue | 29-31 May | Singapore

- Critical Minerals for Defence | 9-10 June | Toronto

- Naval Defense Philippines | 17-19 June | Manila

- ADSE 2026 | 6-7 August | Abbotsford, BC

- Canadian Aerospace Summit | 27-28 October | Ottawa

Other Insights

Canada x IndoPacific [15th Ed.] - Submarine Endgame in Ankara (?), Huge International Acquisition by Canadian Firm, Not So Glorious (But Important) Paperwork & Agreements Move Forward

July 2, 2026

Canada x Indo-Pacific [14th Ed.] Summit Season in Beijing, Wang Yi in Ottawa, CPSP End of the Beginning, Biggest CANSEC Ever

June 4, 2026

Canada x Indo-Pacific [13th Ed.] DSRB to Be Hosted in Canada, Japan’s Export Rule Reforms Continue, CPSP Bid Revisions

May 14, 2026

Defence Market Intelligence for Strategic Autonomy

© 2026 PerceptX Inc.

about

services

Capabilities

News

contact us